If you’ve reached the point in your construction career that you’re ready to move into commercial work, congratulations! That’s a huge milestone to reach and deserves celebration.

There are a lot of considerations you may not have had to think about before if you’re moving from residential construction; however, if you’re prepared and have planned out your strategy ahead of time, you’ll be on the road to commercial construction success in no time.

Have questions about how to get into commercial construction? Here are 5 essential elements that will help you start a commercial construction company with success:

- Figure out your finances

- Make industry connections

- Be strategic about jobs

- Monitor costs and labor

- Choose the right tools

Let’s look at each element in more detail.

1. Figure Out Your Finances

Capital is the foundation of a new commercial construction company’s growth and expansion and determines its entire direction. Without access to capital, starting a commercial construction company is simply not feasible.

During the planning stage of your business, take your time developing a financial management strategy that you’ll follow strictly, but with the knowledge that you’ll need to be flexible and modify that plan when necessary.

There’s no aspect of your commercial construction company that finances will not influence: from your employees’ wages and salaries to your net profit and everything in between. Money management will be the deciding factor that determines which jobs you can and can’t bid on, as well as what kind of risk you can assume.

Odds are, your company’s financial profile will be divisible into two parts: capital and credit.

The Role of Capital and Credit in a Commercial Construction Company

Whether you decide to work with a bank or other lender to finance your company or use your own personal investment funds to start, you must have enough capital or credit to operate until you begin producing profits.

This means you have to be able to cover all of your overhead: salaries and wages, tools and equipment, materials, and operating costs. One of the biggest factors to consider when estimating how much time will be required to make your company profitable – as opposed to merely solvent – is retainage.

What Is Retainage, and How Does It Affect the Overhead and Profit Margins of a Commercial Construction Company?

If you’ve been in the residential construction industry for a while, the idea of retainage might be unfamiliar, but in the commercial world, this practice is common. Even after the project is complete, customers typically hold back a percentage of the total bid – a sum called “retainage.”

The owner of the project holds back the retainage amount, which is typically roughly 10% of the total bid, until the general contractor – your customer – turns over the entire project to them.

So, just because your portion of the work is complete, this doesn’t mean you can expect full payment anytime soon. In fact, it’s not unusual for specialty contractors to wait several months – even years – following the completion of a job before receiving retainage monies.

From time to time, you might be able to make a case for a lower retainage amount during contract negotiations, but you can’t count on that, and you must be prepared for any amount of retainage.

How to Better Prepare for Payment Delays Due to Retainage and Slow Payments

Waiting for that 10% of your total bid might mean waiting for your entire profit margin for a job, and even without considering retainage, payment cycles in the commercial construction industry are notoriously slow. So you absolutely must have the capital to continue operating long after that last job is complete without depending on revenue from it.

This can be a big concern for new commercial operations – how can you finance bigger, more lucrative projects without the money to pay for materials for those projects?

A new solution for contractors that increases capital and improves credit is material financing. Billd, the leading company in this space, pays your supplier upfront for materials and then extends you up to 120-day terms. These extended terms improve your cash flow by allowing you to pay for materials after you’ve been paid for work, opening up opportunities to grow your business and take on more, and larger, projects at once.

Unlike a traditional line of credit that stifles your ability to obtain additional financing and tends to require a blanket lien on your business, Billd does not take up any credit because of its project-based financing approach. With a solution like this, you get breathing room to go after bigger bids without sacrificing stability.

2. Make Industry Connections

The construction industry is extremely reliant on relationships and networking, so be sure you’re prepared to start making those connections with other industry professionals. You should definitely make calls and send emails, but think about going above and beyond those less personal tactics.

Attempt to visit every commercial general contractor in your area and come prepared with business cards and brochures with photos of your best work. Be personable and professional: make eye contact, smile cordially, and explain that you’re just getting started and would like a chance to bid on some of their smaller construction jobs.

Meeting development firm owners and chief estimators in person like this and making a positive impression can give you a substantial edge over other contractors who simply ask to be added to a firm’s bidder list.

Thinking Beyond GCs

When building relationships, don’t stop at general contractors. Introduce yourself to other specialty contractors in the area so you have a solid network of companies who work in complementary trades. You can recommend each other for work and put in a good word for each other, making for a win-win situation.

Also consider your suppliers and vendors in your extended industry network. They can provide information and training on the latest materials available to give you a competitive edge, another mutually beneficial relationship when you give them repeat business.

How to Get Commercial Construction Projects and Sell Your Bid

To find projects to bid on, subscribe to news services and seek out online plan rooms such as PlanHub. Keep an eye on your local builders exchange and your local ABC Chapter. You can also comb through listings on platforms like Dodge and Construction Journal, where you can find projects in various stages, often even in the design phase, so you can get involved and express interest much earlier in the process.

If you’ve made a point of meeting every GC in your area, you’ll begin to see their names appearing on bid lists you find in the news services or online plan rooms. When you do come across a contact you recognize, make follow-up phone calls to let the firm know you’re interested in a job. Use that call to make yourself stand out by asking insightful questions about the job that aren’t readily answered in the RFP.

After the job is awarded, whether you get the project or not, be a good sport and follow up again. Let your contact in the development firm know that if anything changes, you’re available to help.

One word of caution: resist the temptation to go too big too fast. Learn the commercial ropes on smaller jobs first. Prove yourself on these less demanding projects and build development firms’ confidence in your work before you try bidding on more complex jobs.

3. Be Strategic About Jobs

Not only is getting your bid right essential to winning projects, it’s also at the core of success on the actual job. But you also need to make tactical decisions about the jobs you can and want to work on.

Take note of your crews’ strengths; the size, schedule, and complexity of projects in RFPs; and your confidence level as you evaluate. Even if it seems like a job could be lucrative, don’t bid on it if it’s outside your scope, has unclear specs, or is on a schedule that you know your crew can’t meet.

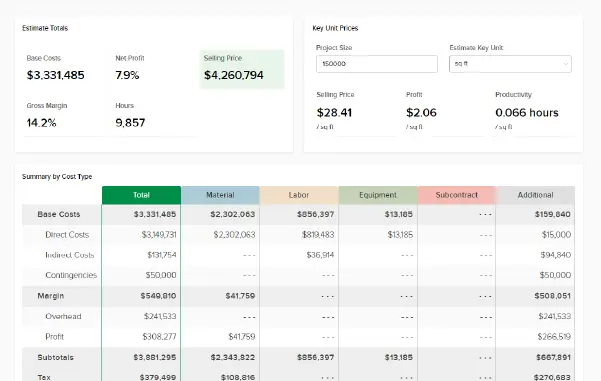

Bidding on jobs that aren’t the right fit can undermine your business’s success when you’re just starting out, and it takes away valuable time that could be spent perfecting bids for jobs that are better suited to your company. Time spent focused on construction cost estimating is a key to your success.

The Importance of Accuracy and Follow-Through

When you identify a prospective project, start out by making sure you understand the elements of the contract for a job, and then begin developing a material takeoff and compiling your estimate. The takeoff and estimate are the essence of your bid. You need to be certain you have all the necessary materials, tools, and equipment for the job. If you find something you can’t afford to contribute, talk to your contact at the development firm about the miss before signing anything.

Double and triple check your estimate before submitting a bid. When you are ready to submit, be sure your proposal looks professional and is clear and thorough. Then, if you’re awarded the job, check your estimate again before you sign a contract.

After signing, prepare your superintendent/crew chief and your crew before stepping foot on site. It’s not uncommon for contractors to do everything right during the construction bidding process and then make the mistake of thinking the planning portion of the job is over. Don’t let that be you.

Instead, focus on the job details and determine what’s required to successfully complete the job before ever sending your crew to the site. If you’re missing tools or you overlook requisite materials, you waste money on idle time – big money in some cases – as your crew waits around for you to get your ducks in a row.

4. Monitor Costs and Labor

Once your crew is on site, immediately begin accounting for every dollar. Especially when it comes to labor and material cost, measure actual progress versus your estimate on a weekly or even daily basis. Getting in the habit of doing this from the beginning sets you up for future success as you grow.

If you’ve failed to estimate a job properly, the mistakes will show up early in your monitoring process, and if you catch them quickly, you can often find new ways to adjust, allowing you to turn the job around before you start accruing losses.

Get your crew set up with and accustomed to using tools in the field that will feed the information you need back to your headquarters. Make sure you know which materials belong where, which crew members should be on site at a given time, and when each phase of the project should occur so you can be prepared.

Reviewing your data regularly during construction helps you avoid a situation in which you wait until the job is finished to tally costs, only to find it’s far too late to make changes that could have kept you in the black. However, you should still make it a habit to conduct a full post-project review when each job is complete so you can fully examine what went right and what problems you encountered. These kinds of reviews help you learn from past mistakes and develop a stronger future strategy.

Considering Your Crew

Something to always keep in mind is that the superintendent/crew chief is the lynchpin connecting you with your crew, and using the right construction superintendent software can help manage tasks and communication more effectively. Hire an experienced super to monitor your labor. A strong, capable leader will make sure your crew shows up on time, is ready to work, and performs to your standards, and that person is worth their weight in gold. Nothing eats away at your profit margin faster than the wrong person leading your crew.

Similarly, consider your hiring practices, benefits, and company culture. Turnover in the construction industry can be high – losing workers and training new folks takes time and resources you can’t afford. Attract and retain good employees – in both the field and the office – by offering competitive benefits, sponsoring continuing education, giving referral bonuses, and more. You’ll be much more profitable if you have a solid, dependable team on your side.

5. Choose the Right Tools

Just as you wouldn’t send your crew to the job site without the right tools and equipment, your administrative team needs the right technology to perform their roles effectively.

The construction industry is infamous for being slow to adopt technology, but with the right programs and applications, you can give your company a competitive edge. However, don’t just choose the first or cheapest app you find – evaluate everything in terms of where you are now, how you intend to grow, and how each option can fit in with your existing workflows.

The purpose of all construction cost estimating technologies should be to save you time and increase efficiency as much as possible.

Takeoffs and Estimating

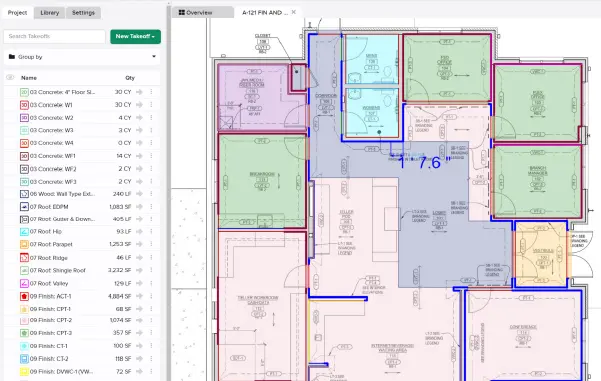

In commercial construction, you’ll be required to perform takeoffs on blueprints to determine measurements and quantities of materials needed for a job. While some companies do these manually with a scale ruler, adopting construction takeoff software from the start will help your team do their jobs at much higher speeds and with more accuracy.

As you compare solutions, look at how user-friendly the software appears. Consider how quickly and easily you and your team can become experts in it, and if there are resources available to answer any questions. Also think about what else you need the software to do: store and organize project documents, allow for team collaboration and field visibility, generate estimates and proposals directly from your takeoffs, and integrate with other tools you’ll be using.

Thoroughly vetting software like this upfront will reduce inefficiencies and redundancies on down the line.

Other Construction Technology Platforms

As you grow, you’ll find you need other technology solutions for organizing and managing projects. Consider project management software like Procore, material and time tracking tools like Raken, and CRM platforms like Followup CRM.

Always look for tools that are cloud-based to allow for team collaboration, mobility, and the best options for integration with your other software.

Build a Foundation for Success

Running your own commercial construction business requires a lot of attention to detail and hard work. But with a little forethought and the right people and tools such as construction software for general contractors in place, you can build a successful business that will grow and flourish!

Ready to take your commercial business to the next level?